Cashflow Lending: A Small Business’s Secret Weapon

Maintaining a healthy cash flow is essential for business success. Discover the tools to help you track, optimise, and stabilise

Monday – Saturday

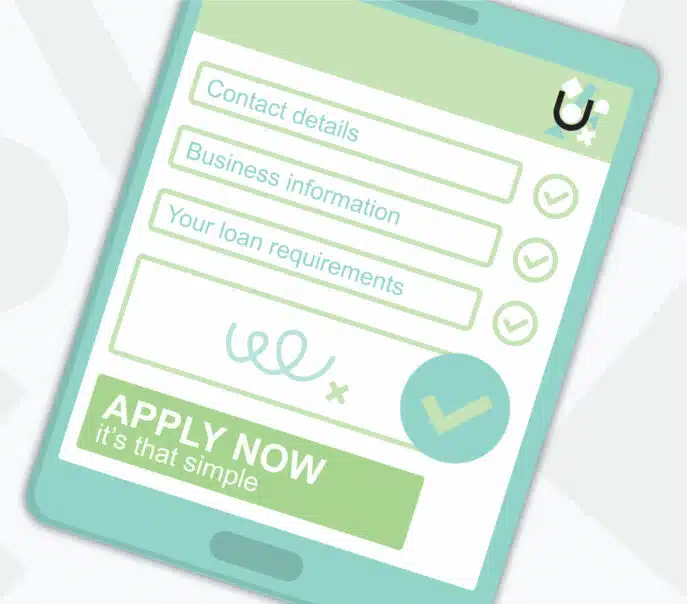

we only need the basics

and fast

get started now

Maintaining a healthy cash flow is essential for business success. Discover the tools to help you track, optimise, and stabilise

Introduction to Business Lending Business lending is a cornerstone for many small business owners looking to bring their business idea